Speculators might make money on it, but the arguments for its usefulness fail completely.

A company called Coinbase has gone public, and Wall Street seems excited. Coinbase is a cryptocurrency exchange—it allows you to buy, store, and trade cryptocurrencies, which are invented kinds of alternative moneys. The most well-known of these are Bitcoin and Ethereum, but there are 4,000 different kinds of these invented new forms of money. (If you’d like to start your own currency, you can.)

Coinbase’s debut on the stock market has been called “the crypto event of the year,” “the coming-out party for crypto,” and it went well. CNN reports that “the groundswell of investor interest is hugely validating for both the crypto economy and the companies that have cropped up to support it.” Vox says that “you should probably start paying attention to bitcoin” because the success of Coinbase shows that it has gone “from nerdy curiosity to mainstream investing opportunity and payment method.” “Once mocked as a tool for criminals and reckless speculators,” reports the New York Times, cryptocurrency “is sliding into the mainstream.”

If it’s mainstream now and we should pay attention to it, it’s a good idea if we try to understand what it is and what its economic implications are. You may have ignored Bitcoin because the evangelists for it are some of the most insufferable people on the planet—and you may also have kicked yourself because if you had listened to the first guy you met who told you about Bitcoin way back, you’d be a millionaire today. But now it’s time to understand: is this, as its proponents say, the future of money?

Many discussions of Bitcoin and cryptocurrency—I am going to use “Bitcoin” and “cryptocurrency” interchangeably for convenience, even though Bitcoin is just a specific cryptocurrency—begin with a long explanation of the blockchain technology that makes it possible. I think for the purposes of talking about what Bitcoin means and does, this is a mistake and a distraction—like having a discussion about the social effects of air travel by talking about how ailerons work. What matters for the purposes of our discussion is that it’s a made-up alternate system of money that, because it’s built on blockchain technology, can be transferred from one person to another without having to go through a bank or a payment processor. Because you don’t have to use a bank, and can easily transfer bitcoin from person to person, it is also “private,” in the sense that you don’t have to give anyone your credit card information or even your name to transfer funds. This makes it particularly attractive to criminals, because it’s sort of like the digital equivalent of cash: easy to hide, tough to trace. And because it’s not tied to a national government, Bitcoin can be used around the world without having to convert currency.

There are many who see this as revolutionary and important. “The popularity of this form of currency is expected to grow exponentially, as it is decentralized, safe, and anonymous,” reads one analysis. “The fact that a huge section of technology-savvy individuals and companies are favoring the decision of using different form of encrypted currencies clearly indicates that the future of Bitcoin or cryptocurrencies as a whole is going to be bright.” Across the internet, you can find blog posts and explainers that tout the benefits and possibilities of this new form of currency. Some people in positions of power agree: “This is the revolution,” said Rep. David Schweikert, a Republican member of the Congressional Blockchain Caucus. “We just have to sell it.”

I’ve been among those who have ignored cryptocurrency for a long time, but Vox has told me I am no longer allowed to, so I’ve read up on it. And I have to say, Schweikert is partly right: “selling it as a revolution” is a hugely important part of why cryptocurrency is succeeding. But as is generally the case when someone is trying to sell you something, the whole thing should seem extremely fishy. In fact, much of the cryptocurrency pitch is worse than fishy. It’s downright fraudulent, promising people benefits that they will not get and trying to trick them into believing in and spreading something that will not do them any good. When you examine the actual arguments made for using cryptocurrencies as currency, rather than just being wowed by the complex underlying system and words like “autonomy,” “global,” and “seamless,” the case for their use by most people collapses utterly. Many believe in it because they have swallowed libertarian dogmas that do not reflect how the world actually works.

Let’s start with the basic promise, that of being “decentralized, safe, and anonymous.” People like the word decentralized. I like it a lot myself. Nobody likes centralized authority. You know who liked things centralized? Stalin. But what does the word actually mean? In this instance, it means that financial transactions are peer to peer, rather than going through your bank or a processor like PayPal, and that there is no central bank altering the money supply, as there is with the U.S. dollar. Many of the pitches for Bitcoin begin by emphasizing its decentralized nature.

- “Unlike services like Venmo and PayPal, which rely on the traditional financial system for permission to transfer money and on existing debit/credit accounts, bitcoin is decentralized: any two people, anywhere in the world, can send bitcoin to each other without the involvement of a bank, government, or other institution.” — CoinBase

- “You Are in the Driver’s Seat — One of the best things about cryptocurrency is that, unlike virtually any other type of money retaining system (save for a wall safe or your wallet) you totally own it. Think about it: most traditional liquid asset systems – banks, credit unions, brokerage houses, or even high tech ones like PayPal – take control of your funds and leave you subject to their terms of service. If they decide that you have violated those terms, they can suspend your account. They can change their terms of service, and cause you to have to pay more or receive fewer funds for important transactions. With cryptocurrency, you retain all of the funds on hand, so to speak, digitally, with no third party involvement; the only one who can change the terms of your cryptocurrency use is YOU.” — Nasdaq

- “[Cryptocurrencies] enable financial transactions quickly, inexpensively, and more securely. Decentralized crypto does everything that traditional fiat money does— and far more—because it is global and not subject to totalitarian government controls or any third-party interference.” — “How Does Cryptocurrency have Value and Why Should I Care?”

There are recurring themes and bits of rhetoric in the pro-crypto propaganda. (A term whose use is more than justified.) It’s about freedom. It’s about getting the government off your back. It’s about getting middlemen and third parties out of your transactions. It’s about control, autonomy, empowerment.

But if we get past the rhetoric and think about the implications for the average person, it’s not clear that we are actually meaningfully improving “freedom” in any but the most abstract, theoretical way. For the average currency user, why is it so important to get rid of banks and the government and these suspicious-sounding “third parties?” Yes, we all hate bankers, but is the tyranny of Venmo so oppressive that we should shed the U.S. dollar entirely and begin trading in an alternative currency? Yes, it’s true that if you bank with a credit union, you can think of it as “surrendering control of your assets to a credit union.” The crypto-enthusiasts raise the specter of violating the Terms of Service and having your account suspended. I don’t know about you, but this has not happened to me, ever. I’ve gone overdrawn and had to pay stupid fees (fees they hilariously euphemize as “overdraft protection”). I’ve had my debit card stop working because the bank thought a purchase was fraudulent and it wasn’t. But the main problems that people have with their banks and credit unions do not have to do with the bare fact that an institution is holding their money.

In fact, when we examine whether Bitcoin can function usefully as an alternative currency for the average person, we see that all of the grand claims for it fail entirely. Using it does not create greater security or safety for one’s finances. It does not free one from the oversight of the government. It is not convenient or free. Its volatility makes it functionally useless as a currency. Furthermore, these drawbacks are not fixable; they are products of the very concept itself. There is a reason that you are not using Bitcoin for transactions, even though it has been around since 2008. It is that while Bitcoin is based on an interesting technological innovation (blockchain), it is not a good idea for an alternate money system, due to its dependence on several libertarian illusions.

The “Security” Illusion

A lot of the pitches for cryptocurrency suggest that having your money in a bank makes it less secure, because a Third Party is being entrusted with it. So much of the propaganda is about “security” and how payments made with Bitcoin are more Secure than those made with PayPal, because you don’t have to provide identifying information and the transactions do not involve “third parties.” One site lists on the “ways cryptocurrency will help you” the prevention of fraud, because “individual cryptocurrencies are digital and cannot be counterfeited or reversed arbitrarily by the sender, as with credit card charge-backs.” From the European Business Review:

- Strong security: When you perform the transaction in cryptocurrency, you cannot reverse it. There will be a reliable encryption technique used throughout the cryptocurrency transaction process to protect from hackers and tampering the information.

- Bitcoin is irreversible. Bitcoin is like cash, in the sense that transactions cannot be reversed by the sender. In comparison, credit cards, conventional online payment systems, and banking transactions can be reversed after the payment has been made—sometimes months after the initial transaction—due to the centralized intermediaries that complete the transactions. This creates higher fraud risk for merchants, which can lead to higher fees for using credit cards. Bitcoin is private. When paying with bitcoin, there are no bank statements, or any need to provide unnecessary personal information to the merchant. Bitcoin transactions don’t contain any identifying information other than the bitcoin addresses and amounts involved. Bitcoin is secure. Due to the cryptographic nature of the Bitcoin network, bitcoin payments are fundamentally more secure than standard debit/credit card transactions. When making a bitcoin payment, no sensitive information is required to be sent over the internet. There is a very low risk of your financial information being compromised, or having your identity stolen. — Coinbase

- Safety Advantages of Bitcoin: Bitcoin already boasts several security benefits over traditional currency. When you buy something with a credit card, a third party pulls the funds from your account (known as a pull transaction). Bitcoin, on the other hand, uses push transactions, where you hand the payment over yourself. With pull transactions, hackers can pretend to be you and get your bank or credit card company to move money for them. With a push transaction, though, they need access to the money itself, not just your personal information. That’s not where Bitcoin’s safety features end, either. Bitcoin leverages the blockchain, so it’s decentralized and immutable. Some scholars suggest using Bitcoin to prevent identity theft because the system is so secure.

- Fraud reduction – A payment made with bitcoin cannot be reversed after the fact. This is different from credit card payments, which can be reversed using chargebacks, a feature often exploited by fraudsters.

This really does essentially amount to lying. It depends on a confusing definition of “security” that misleads people into thinking they are somehow less likely to be scammed if they transact in cryptocurrency. In fact, because there are no trusted third-party institutions, if someone tricks you into a fraudulent transaction, there’s nothing you can do about it. Credit card payments, as noted above, can be stopped and reversed. But Bitcoin payments can’t. Once the money’s gone, it’s gone. This is touted as a feature because it helps merchants: if a customer gives the merchant money, the customer can’t take it back if they don’t like the merchant’s product. But most of us aren’t merchants. We’re consumers. The fact that transactions are “irreversible” may reduce the fraud risk for the merchants, but it has a flipside, which is increasing fraud risk for the customer. It’s not rational for consumers to surrender their right to stop a charge, and it’s not accurate to describe this as “fraud reduction.” In fact, it’s just shifting who suffers the consequences for fraud.

In fact, it turns out that there are a few advantages to having those “third party intermediaries” from whose tyranny cryptocurrency promises to help us escape. I grumble when my bank stops a payment on my credit card thinking it’s fraudulent, but I like that my bank has fraud protection. (Thanks, federal law, for putting a set of rules in place saying when banks are liable for fraud, thus incentivizing them to catch fraudsters.) Bitcoin’s decentralization means nobody is looking out for you. Nobody. Getting rid of a third-party institution that offers fraud protection is not making your payments “more secure,” it’s making them less secure. The use of “security” here means narrowly “it’s guaranteed that the person who is supposed to receive the money will in fact receive it.” But from the consumer’s perspective, the “security” of transactions is holistic, meaning that it doesn’t matter whether one aspect of the transaction is secure if there are many other aspects that are highly insecure. Often, if you look closely, there are serious qualifications and caveats about the “security” benefits—Bitcoin “can represent a safer alternative to fiat trading if the right conditions are met (namely implementing an effective blockchain analytics practice to remain safe from errant typologies that exist on the blockchain) [emphasis added.]” How likely are ordinary people to even learn what these words mean, let alone know whether they’re implementing them effectively?

Indeed, those without technical know-how are easy to steal from in the world of cryptocurrency. Bitcoin.org warns of scams including: “Blackmail, Fake Exchanges, Free Giveaways, Impersonation, Malware, Meet in Person, Money Transfer Fraud, Phishing Emails, Phishing Websites, Ponzi Schemes, Pyramid Schemes, Prize Giveaways, Pump and Dumps, Ransomware, and Scam Coins.” The same websites that tout the unbelievable security benefits of using Bitcoin, the way it can stop identity theft, then warn of Bitcoin identity theft. The “anonymity” of Bitcoin transactions may help you. But it may also help a scammer take advantage of you. For most everyday use, you don’t want anonymous transactions. You want there to be a record of what you paid and who you paid it to, so that they have a legal obligation to give you what you paid for, and it can be shown that they received the money.

The “Privacy” Illusion

This is not to say that anonymous transactions offer nobody any benefits ever. The most obvious class of people who might need it are those operating outside the law. This includes drug cartels and white collar criminals, but it also includes criminalized industries like sex work. Marxist dominatrix Mistress Magpie told the Nation that while “the majority of her clients are not well versed in digital currencies,” cryptocurrency could offer a way to operate “furtively under capitalism, in a way that might not be needed in a more open socialist society.” This is an argument for having an anonymized digital currency of some sort in the here and now, but it should be noted that it means we should be building a world in which cryptocurrency is obsolete, because people aren’t prosecuted for victimless crimes.

But does cryptocurrency actually offer these benefits anyway? In fact, anyone who starts using Bitcoins and thinks they’re making untraceable transactions is wrong. The very idea that Bitcoin is “anonymous” is highly misleading. Coin Insider comments that “there is no surefire way to maintain one’s anonymity when using Bitcoin.” The Wall Street Journal, discussing how Bitcoin scammers operate, says that while it is a “cat and mouse game” between law enforcement and the scammers, more sophisticated tracking tools are being developed all the time, and the one thing we do know is that the scammed will likely never see their Bitcoin again. In fact, the idea that cryptocurrency is even particularly useful for crimes may be false. The RAND corporation notes that despite the “perceived attractiveness of cryptocurrencies for money laundering purposes . . . an estimated 99 per cent of cryptocurrency transactions are performed through centralised exchanges, which can be subject to AML/CFT [Anti-Money Laundering/Combating the Financing of Terrorism] regulation similar to traditional banks or exchanges.” So nearly all transactions are facilitated by third parties, namely companies that act as “exchanges,” serving as an intermediary that facilitates transactions. These companies are subject to subpoenas just like any other. In fact, if you go on Coinbase—the exchange that is mainstreaming the use of cryptocurrency by making it easy to use—the very first thing you are asked is to verify your identity, giving your name, phone number, the last four digits of your social security number, etc.

Unless you are a highly sophisticated actor, you are not going to be keeping the government from being able to figure out if you made a particular payment to a particular person, because your use of cryptocurrency will be through a legitimate company that complies with U.S. financial regulations.

If you are a savvy enough individual to avoid the exchanges, you may not experience this. But it is a vanishingly small number of people who need so much more privacy than that which can be offered by any bank, and are doing legitimate (if unlawful) things such as trying to subvert U.S. sanctions, and cannot operate in the even safer medium of cash, and are sophisticated enough to figure out how to avoid all the obvious pitfalls by which they can be caught and prosecuted. If you are an ordinary consumer, the privacy difference is going to have almost no practical effect, and so there is no reason for you to use a cryptocurrency rather than just a currency. Bitcoin’s advantages are far more likely to help the sophisticated person trying to steal your money than they are to help you keep your money safer than it would be in Chase Bank.

The Convenience Illusion

The European Business Review cites “easy transactions” as a key draw for cryptocurrency. Perhaps, though not really easier than existing payment processors that do not require you to convert your money into an arcane new currency and back again to use it. But importantly, cryptocurrency also offers new and scary ways that you can actually lose all of your money, which should certainly factor into an assessment of how convenient it is. A Wall Street Journal analysis in 2018 found that 20 percent of all Bitcoin tokens were lost and probably unrecoverable, because if you lose your PIN for your Bitcoin wallet, you can never access it again. “Unlike an ATM PIN, this password can’t be recovered easily, since there is no bank to retrieve it,” says the Journal. Investopedia says that “the reason for this has to do with the structure of cryptocurrencies and the emphasis they place on privacy and security.” One guy who had $220 million in Bitcoin, because he bought early and the value exploded, had no way to access it because he had lost his PIN.

Once again, we see the word “security” being used in a strange way. Security, for most of us, means the reduction of the risk that our money will disappear. If you lose access to your Bitcoin, a “crypto hunter” can help you try to track it down, but one of the great things about having a bank is that when I lose my PIN, I just call the bank and they let me into my account. I don’t want this “third party” to disappear, even for an additional kind of privacy that means nothing to me practically speaking. The trade-off offers me nothing.

In fact, I tried using Bitcoin once, and I was struck by how extremely inconvenient it was. I kept asking myself: “why would I ever want to use this?” Of course, companies like Coinbase offer ways to buy, sell, and transfer cryptocurrency swiftly. But they’re a centralized third party administrator! Institutions like banks could continue to arise, because they make it easier for unsophisticated users to navigate the complicated world of crypto. But then we’re just recreating banks, defeating the whole purpose of using cryptocurrency in the first place. As Doug Henwood notes:

[W]ith no regulator, no deposit insurance and no central bank, [fraud and theft are] inevitable—it’s just tough luck. Introduce regulators and insurance schemes, though, and Bitcoin will lose all its anarcho-charm.

This means that Bitcoin is caught in a paradox: if the reasons why you shouldn’t use it are dealt with, the whole purpose of using it in the first place is defeated. If Coinbase becomes just like PayPal or Venmo, what earthly reason is there for me to convert my dollars into Bitcoin using Coinbase, and transact with someone who will then have to convert the Bitcoin back to dollars (at least if they want to use it almost anywhere)? What added value is being provided by the alternative currency? I’m sure private services will pop up that can help me “implemen[t] an effective blockchain analytics practice to remain safe from errant typologies that exist on the blockchain,” which I’m told I need to do. But then I’m paying someone to help me solve a problem I didn’t even have before, and I don’t get convenience and am still giving a cut to a middleman-type-entity, in this case the person who helps me—the oblivious non-techie—from accidentally screwing up the use of this complicated currency.

Many of the supposed advantages of Bitcoin, then, are actually disadvantages. Having a fixed money supply with no central bank means there is no regulator who can help stabilize the value of the money. As I was writing this article, the value of Bitcoin plummeted 10 percent in 24 hours. If the U.S. dollar lost 10 percent of its value in a single day, people would be comparing this country to Zimbabwe. Yet Bitcoin is intended to be better than fiat currency! The biggest illusion at the heart of the crypto-fraud is that markets can be self-regulating and stable. In fact, markets are created by states and societies, exist within frameworks of law, and must be tended, fed, and cared for by governments if they are to function. Bitcoin pretends to shed the very feature that makes money work—adapting to and conforming social and political institutions and rules. Instead, it relegates its own political judgments to a rigid algorithm, which makes it both unable to respond to the changing world and completely outside the control of the society that must accept and use it.

Alternate Currencies Need A Reason To Exist

In fact, let’s imagine a scenario that will help us see how silly this all is. Let us imagine that I come up with a scheme to revolutionize how people transact. I have invented a new form of currency called Nbucks. They are slips of paper with my face printed on them. I set about trying to encourage businesses to pay people in Nbucks and trying to encourage people to buy them from me. (I sell each Nbuck for $1.) “Why,” you might ask me, “should I transact in Nbucks instead of U.S. dollars?” I have ready answers for you. First, the Nbuck is not controlled by the U.S. government. I am only going to make 1,000 total Nbucks, so the money supply is fixed. Using Nbucks you can transact with people without going through a bank or paying a fee. And you can transact with people in other countries who take Nbucks, without having to go through the pesky process of converting to the local currency. With my special Nbuck app, you can transfer your Nbucks to other people at any time without any fees. Through Nbucks, I tell you, we will free ourselves from centralized government control of the money supply. You will have total autonomous control of your money, for while I set up the mechanism to make the initial Nbucks, once they’re made, my role ends and we just kind of see what happens with it.

Now, at this point you might ask a few questions about my nifty system, such as:

“You say I can transact with other people who use Nbucks, but how many people use these things?”

“0.01 percent,” I answer, “but it’s growing all the time.”

“I see,” you reply. “And so what is the advantage of having a currency I can barely use? Why would we switch to this system when we have dollars?”

“Well, it’s free of centralized government control. And banks. Plus its value is going up all the time. An Nbuck worth $1 today will probably be worth $5 next year, because there are only 1,000 of them and demand for them is increasing.”

You will notice that my answer seems like a good argument for buying them as a speculator, but it is not an argument for why they are useful as a currency. In fact, it seems to cut against their usefulness, because it’s hard to transact if the value of the money is changing unpredictably all the time. In fact, while it’s clear that Nbucks could function as an alternative currency system if enough people switched to them, it’s not clear why anyone would switch to that system. If I convince enough people that these things are valuable, they will indeed be valuable—just like Beanie Babies became valuable because people were convinced of their value—but how is what I’m offering useful to the average consumer as a currency in which they should conduct transactions? In fact, it’s essentially useless for the typical person, because they can’t buy much with the money, it’s inconvenient to keep converting dollars to Nbucks and back again, and their value is unpredictable.

A portion of people in society could switch to using glass beads instead of U.S. dollars. The beads might even be more difficult for the government to trace. The beads might even become extremely valuable. But none of this is an argument for switching to a glass bead economy, or for any given individual to embrace beads. Likewise, Bitcoin could be adopted more and more widely. Cryptocurrency does seem to be taking off. I’m not saying the trend won’t continue. I am saying it doesn’t solve the problems it says it solves, and that ordinary consumers do not stand to gain much of practical value (and have a lot to lose) from using cryptocurrency. There is no value added unless you are a dissident/outlaw, and even then, you’re better off using cash if you can.

Why, then, does the value of Bitcoin keep going up and up? Why is Coinbase so valuable? Because people believe in it. Or they believe they can make money off it. And people have made vast fortunes off it. You might buy some Bitcoin because you think it’s going to keep gaining value, and you might not be wrong. Hell, GameStop stock went up and up for a while; speculators can speculate on anything. The irony with Bitcoin is that the better it is as an investment, gaining value rapidly, the worse it is as an actual currency, because its worth is unpredictable. (Doug Henwood outlines some of the other reasons Bitcoin fails as an actual currency here.)

Now, personally, I don’t care very much whether people want to use cryptocurrency, though as a believer in consumer protection I would warn anyone considering it to be very, very careful. It does interest me, however, because the people who believe in it seem to embody the wishful thinking common among free market libertarians who think that freedom from “the government” is automatically good. In reality, while plenty that the government does is oppressive (e.g., mass incarceration) some of it is extremely useful (e.g., FDIC insurance). Much of what banks do is odious, but a credit union can be an extremely useful institution. Regulators are good. The Consumer Financial Protection Bureau is good. Being unable to be traced by the government is sometimes good. But sometimes, as in the case of rich tax evaders and people who have stolen our savings, we want things to be traced.

Many of the problems cryptocurrency seeks to solve can be dealt with through means that do not involve trying to jettison the U.S. dollar. For example, one of the touted virtues of cryptocurrency is that it is fast and there are no transfer fees. In reality, transfers are often quite slow and fees can be exorbitant. But public digital dollars and consumer accounts at the federal reserve could reduce the problems that come with bank account access, minimum deposit fees, slow transfer speeds, ATM fees, etc. These problems aren’t getting solved with Bitcoin—Bitcoin ATMs are popping up around the country, but turning your cash into Bitcoin or your Bitcoin into cash costs money. (My bank refunds ATM fees, meaning that using Bitcoin ATMs would be a very stupid thing for me to do.) If the infrastructure to make Bitcoin convenient and usable has to be built by the private sector, then it will try to squeeze money out of consumers. The promise of “free transactions” with Bitcoin is, like so many other capitalist promises, illusory. The question of whether people will be exploited by the finance industry is not a question of whether they’re using U.S. dollars or some alternate currency, but whether the institutions they’re relying on operate in the service of the public interest or of private interests.

When I say that cryptocurrency is a fraud, let me be clear: I don’t mean that it can’t work as a currency. Anything can work as a currency, though the better ones have predictable values so that a hamburger costs the same on Tuesday as it does on Wednesday. I mean that for most ordinary people, the answers offered to the question “Why should I use cryptocurrency?” are deceptive or nonsense. Instead of being taken in by the words privacy and security—which are good things that people indeed want—we have to look at whether these things are actually being delivered to consumers and if the difference is meaningful and worth the trade-offs. What are you really getting, what are you giving up to get it, and is the rhetoric of crypto-propagandists actually fulfilled in the real-world experience of using it? This total lack of an actual argument for why it’s good is why Warren Buffett has long thought it’s a worthless delusion and refuses to go near it. Buffett doesn’t doubt that people might make money on it, but he sees that the claims made for it simply don’t hold up. (Buffett prefers to invest in more tangible assets like predatory mobile home companies.)

What About The Developing World?

When I point out that the U.S. consumer has no reason to adopt Bitcoin as a currency, the most forceful (and most left-ish) reply I get is that while this may be true for the U.S., cryptocurrency can offer wondrous advantages to unbanked people in the developing world. If you are in a country whose currency is unstable or where international wire transfers are prohibitively expensive, Bitcoin might be helpful. They point me to news stories about how people in certain African countries are increasingly using Bitcoin for certain purchases.

Let us note that there is something to the argument that there is a class of people for whom Bitcoin may be better than existing alternatives for certain purposes. I think this class of people is very limited, however. People in the developing world don’t like losing 10 percent of the value of their wealth overnight any more than people in the United States do, and to the extent that Bitcoin offers advantages, it does so only because the existing alternatives are so bad.

It is true that in some places, international wire transfer fees are outrageously expensive. Sending Bitcoin is not free, and you have to convert it back into cash if you want to actually do anything with it, but it might be better than the alternative, in some places, for now. But if wire transfer fees do come down in the next few years, that advantage will be lost. The argument that Bitcoin will be globally helpful depends on assuming that the existing banking industry is not going to succeed in expanding its reach.

During an economic crisis, or in places where bank failures occur, Bitcoin might be more helpful. In Venezuela and Zimbabwe, there may be an argument that despite cryptocurrency’s disadvantages, people are less likely to lose their shirts by using it. But what this means is that we have got a case the cryptocurrency helps those who:

- Live in certain countries, mainly clustered in Africa, and need to conduct international wire transfers within the next few years;

- Live in economically unstable countries and cannot keep their wealth in a foreign bank .

To the extent that Bitcoin is the “future of money,” then, it is only the future of money in situations of extreme crisis or deprivation—I suspect a lot of the pro-crypto people who understand its present-day uselessness are betting on a future collapse of the global economic system, although I think they overestimate the chances that Bitcoin itself could keep functioning effectively in such a nightmare scenario (someone has to maintain the actual wires).

This argument for the usefulness of Bitcoin actually makes me think of the Segway. The Segway was intended to revolutionize transport, and its technology was innovative and impressive and cool. But the Segway did not revolutionize transport. It did end up being used for a lot of tour groups, however. Bitcoin seems similar. Blockchain is clearly impressive. But that doesn’t mean Bitcoin will revolutionize global commerce. Like the Segway, however, it may develop some niche application for some small group of people for whom its disadvantages do not outweigh its advantages.

Even those people, however, may eventually find their way back to government currency. Many governments are starting to explore the possibility of offering digital versions of their fiat currency through central banks. These kinds of accounts would make transfers easier and cheaper and give many more unbanked people the ability to store their wealth in a secure place. (The prying eyes of government will still be a problem.) We shall see whether progress is made quickly on this front. If not, it may well be true that swathes of the developing world resort to crypto funny-money. But if so, it will be because it is the least-worst option.

Crypto-Hype Won’t Stop

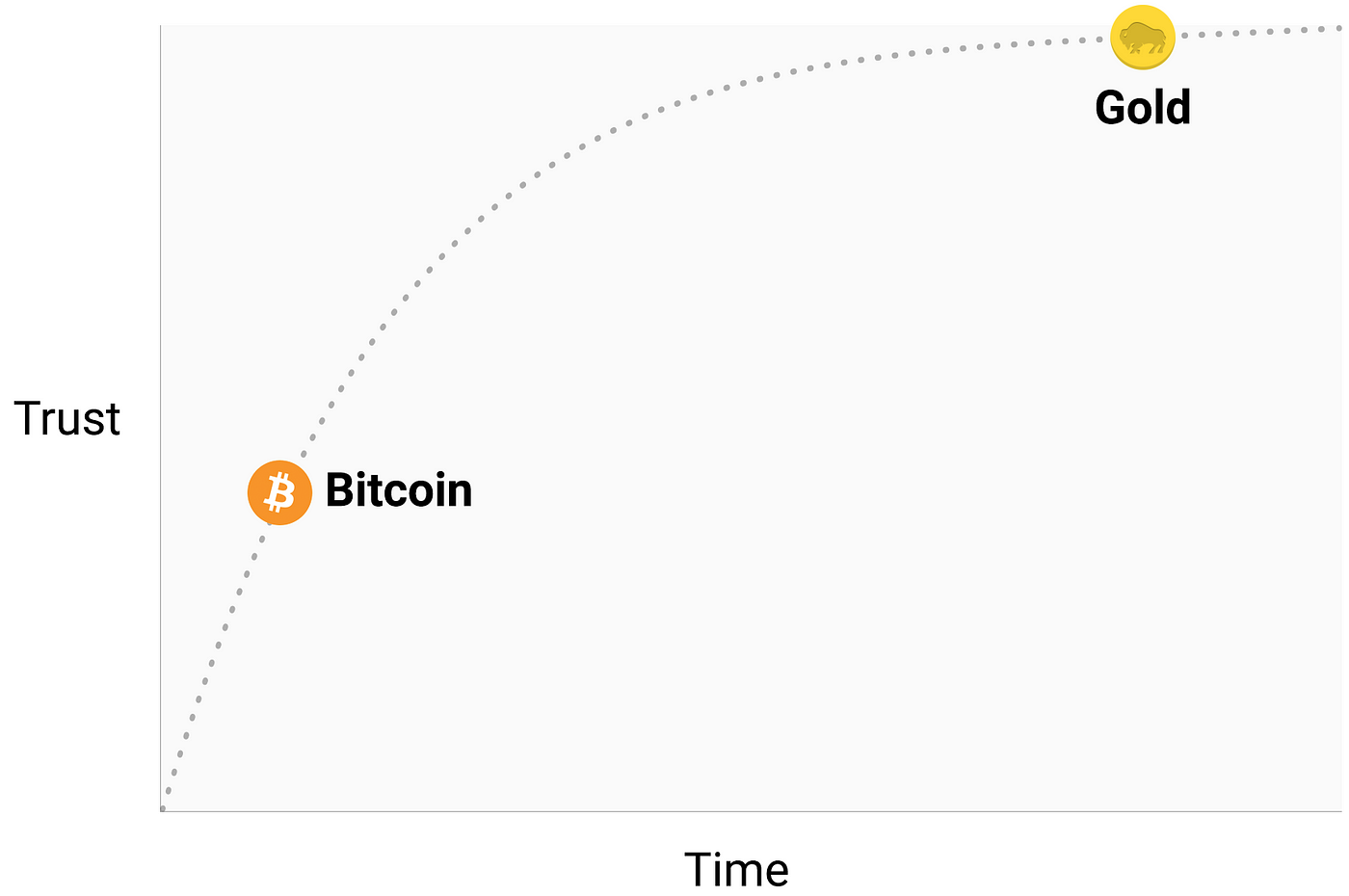

If you want a good example of nonsense crypto-hype, have a look at this pseudoscholarly masterpiece by Vijay Boyapati called “The Bullish Case For Bitcoin.” It was recently promoted by Twitter CEO Jack Dorsey, and even re-tweeted by progressive congressman Ro Khanna. (Khanna is a crypto-booster, saying its decentralization “provides a check against economic mismanagement” and is “the next digital frontier.”) Boyapati provides a case that Bitcoin is a good investment (using some deeply amusing graphs), but he also tries to show that it has strong potential as a currency.* He lists the supposed qualities a currency needs and shows that Bitcoin is better than the US dollar (fiat money) on most accounts:

Of course, half these ratings are false and most of them have nothing to do with what people need from money in the real world. The fact that U.S. dollars are not “scarce,” in that the government can create more of them, is actually a good thing (for one thing, it means the money supply can grow with the economy; for another, it means we can stimulate the economy through putting new money into it). Boyapati says dollars are less “durable” than Bitcoin, because “many governments have come and gone over the centuries, and their currencies disappeared with them,” which is true as a historical fact but tells us nothing whatsoever about the future of the dollar. Note that Boyapati does not include in his fake ratings “spendable” (i.e., can you actually use it for anything) because Bitcoin would be crushed on this. Boyapati does invoke some fake science—like the “Gartner hype cycle”—to support his belief that Bitcoin’s future is bright. Look at this magnificently stupid graph designed to show that Bitcoin will eventually be as trusted as gold:

You should expect to hear more of these sunny pro-crypto arguments, because those who are heavily invested in cryptocurrency will be working hard to try to trick people into thinking it’s in our best interest to embrace cryptocurrency. Boyapati’s pitch looks like prophecy, but people who are invested in Bitcoin need to be making these prophecies all the time, as emphatically as possible, because for the currency to succeed people must join in the collective belief that the prophecy is true. (More cynically, for people speculating on Bitcoin to maximize their return the demand for Bitcoin must keep rising.)

The world of cryptocurrency is one in which wily and technologically sophisticated people can easily take advantage of less financially or technologically savvy people—and the people making the arguments for it happen to be exactly the ones who can navigate this world well and make money in it. It is the libertarian paradise, a Wild West where everyone is trying to take each other’s money and there are no publicly-controlled entities looking out for the common good. Current Affairs contributor Andrew Ancheta comments on the ugliness of this world, which has come to replicate the worst aspects of existing capitalism: “crypto-capitalists have reinvented the finance industry’s fractional reserves and derivatives, private interests began trading votes and carving out monopolies, and rent-seekers found ways to extract surplus value, all while trashing the environment and finding new ways to concentrate wealth at the top.”

Trashing the environment? Oh yes, I haven’t even told you about the fact that Bitcoin’s “autonomy” means it has to deploy a silly system that ends up using the same amount of electricity as an entire country, and the problem is getting worse. Cryptocurrencies vary in their wastefulness but Bitcoin “is only likely to consume more and more electricity over time” despite already using an “unfathomable amount of electricity.” Vitalik Buterin, the computer scientist behind Ethereum, the 2nd most popular cryptocurrency, admits that it’s an unnecessary “huge waste of resources.” Ethereum has promised to improve the system in a way that will reduce these destructive side effects. But what it means is that at the moment, cryptocurrency is imposing a giant externality on everyone: the failure to put a price on carbon emissions means that polluters can essentially steal from the rest of us.

If the energy problem can be solved, cryptocurrency will become somewhat benign and useless rather than actively destructive and useless. This will be used by some to convince you that you ought to start thinking about using cryptocurrency, and merchants ought to accept it. Be careful, because this fad could genuinely result in portions of the economy switching to a system that disadvantages consumers, on the promise that it will solve problems that could easily be solved through effective public institutions, if we were able to exercise our collective political will. The need for security, privacy, and easy money transfers is real, but the promise that a new form of money will rein in the surveillance state or free us from profiteers is illusory. Only strong—yes, sometimes centralized—democratic institutions can do that.

* Interestingly, Boyapati cites Bitcoin’s high transaction fees as a feature rather than a bug: “A recent criticism of the Bitcoin network is that the increase in fees to transmit bitcoins makes it unsuitable as a payment system. However, the growth in fees is healthy and expected… A network with ‘low’ fees is a network with little security and prone to external censorship. Those touting the low fees of Bitcoin alternatives are unknowingly describing the weakness of these so-called ‘alt-coins.’” As you can see, this successfully makes the case that high fees are unavoidable, but it also undermines the reasons why any sane person would use this as currency rather than a speculative investment.

{kind=link}